I recently announced that I will no longer be publishing income reports here on Leaving Work Behind.

I recently announced that I will no longer be publishing income reports here on Leaving Work Behind.

Reactions were mixed — from disappointed to supportive (and combinations of the two). While I knew it was the right decision for me, I was curious to observe what you guys thought.

What I found most interesting was that not one person commented on how no longer publishing income reports might affect my business. After all, I said in the post that I would no longer be keeping track of the money I make on a month-to-month basis. I’m surprised that no one picked up on that and called me crazy. After all, what kind of businessman doesn’t know how much money he’s making?

In this post I want to reveal the only figure that really matters to me and explain how my income reports have been misleading me for a long time.

The Only Figure That Matters

I wasn’t even keeping track of the only figure that matters until I started thinking seriously about stopping income reports. In fact, my income reports were actually preventing me from seeing the real truth of my financial situation.

So what is the only figure that matters? Simple: total liquid capital — i.e. the amount of freely available cash you have in your bank account(s).

On the 20th of every month, I take five minutes to add up the money in all of my accounts:

- My personal current account

- My personal savings account

- My business current account

- My two PayPal accounts

I exclude any money I put aside for tax. If I had any money tied into investments, I would exclude that too, but I would include any income produced by those investments.

I log these figures in a spreadsheet and compare the total to the previous month. If this month’s figure is comfortably higher than last month’s, I’m happy. If the figure is getting a little too close for comfort or is in the red, I know I need to take action.

More than any other, this figure represents reality. It’s not just a number on a page (like all of the numbers I had in my income reports); it represents the actual cash I have in my bank. It represents my financial security — my ability to live my life in its current guise.

In my opinion, any figure which distracts you from your total liquid capital should be discarded. Nothing is more important.

Money: What Really Counts

People are obsessed with income, but that is only one piece of the puzzle. When it comes to financial security and preserving your way of life, all that truly matters is your liquid capital, which is directly related not only to what you make, but what you spend.

If someone publishes an income report saying they made $20,000 in a month you can be impressed, but what if they spent $30,000 on a new car too? They’re $10k in the red for that month now. Yes, big-figure income reports are impressive, and few people are going to drool over how much money you saved in a month, but those of us in the real world should apply just as much effort to reducing our outgoings as growing our income — especially considering that reducing your outgoings is typically far easier.

I have been hiding from this truth for many months; my income reports have kept me ignorant. Thankfully, with them behind me, I can now see the reality of my real financial situation from month-t0-month.

Ignorance may be bliss, but I’m glad to have had my eyes opened.

But What About Growth?

Although I often say that making money isn’t the most important factor when it comes to running my business, it is still important to me. More money means more security and a greater freedom to mould my business into something that I find as rewarding as possible.

So although I may not be keeping an eye on my specific income figures, I will continue to observe my business’ performance in terms of profit — albeit on a more intuitive level.

My method is quite simple. I can split my business’ main sources of income into three piles:

- My writing business

- Affiliate income (mainly Westhost)

- Product sales (i.e. Paid to Blog)

All I need to do is keep an eye on those figures. I’ll periodically check in on how each income stream is doing (by taking a quick peek at sales figures / projections), and if I spot that anything is awry, I’ll take steps to improve the situation. That’s it.

Could I improve my bottom line by keeping a closer eye on the numbers? Almost certainly. But as a business owner, one can always make more money — one of the key determinants of your profitability is when you choose to say “enough is enough” and apportion more time to other parts of your life.

That’s all I’m doing with my approach. I suppose the only difference is that my relatively laissez-faire attitude — born out of non-profit-oriented priorities — is somewhat unusual.

A Shocking Discovery

Now let’s talk about how my income reports have been “wrong.”

It actually took me stopping income reports to discover that my financial situation isn’t quite as rosy as I realized. Ironically, those income reports were shrouding the truth: that my liquid capital hasn’t been growing as readily as I thought.

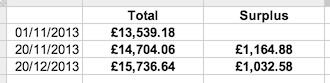

Here’s a snapshot of the figures since I started running them:

On the surface the growth may seem pretty healthy — an increase in liquid capital of ~£2,200 (~$3,500) in less than two months. However, it should be put into perspective. Not only is the surplus gross of tax deductions (and therefore far smaller on a net basis), my income reports had led me to believe that my growth would be more impressive.

For example, my final income report in October announced total earnings of ~$7,500 (~£4,600). My budgeted outgoings are approximately £2,600, which means that my liquid capital should have increased by £2,000 in that month alone. That projection is not reflected by the figures above.

The overriding issue is that my projections are just that: projections.

Firstly, I know that what I budget to spend may not be what I end up spending. Secondly, because of the vagaries of accounting and financial transactions, my income reports did not necessarily reflect the amount of money that ended up in my account in any given month.

The explanation lies partly in the way that I created my income reports: a combination of cash and accrual accounting. I would add up the amount I invoiced to clients, plus what my affiliate partners’ reports said for the month, plus total information product sales, minus cash expenditure in that month.

For the most part, the income I reported would eventually end up in my account, but not necessarily in that month. For example, there is a 90 day holding period on Westhost affiliate payouts, so if I generate $1,500 in sales in January 2014, I won’t get it until April 2014.

The other reason why my income reports did not reflect the money that hit my account was currency charges. I receive the bulk of my money in US$ through PayPal, and they take a very healthy piece of the pie for converting that money into pounds sterling (my native currency). It really hurts to be “double taxed” by PayPal on transaction fees and conversion fees, but that’s the reality of the situation I face.

The moral of the story is this: income reports can be misleading, but the amount of liquid capital you have in the bank can’t. It’s the only truly “honest” figure available.

So What Now?

I’m not panicking. You should know by now that panicking isn’t my style 😉

After all, I’m still making money, and my income reports were broadly correct — while you can take off an amount for conversion charges, the income reported from one month to the next will hit my account eventually.

I now have a far greater awareness about my money than I did before and as such am in a position to make more informed choices — relating to both my income and expenditure. It’s not sexy, but there, I said it.

At the end of the day, money is only money. It’s often put up on a pedestal, but there is more to life. Don’t get me wrong — we all need money to live in relative comfort and security, but earning more than that is a pleasure often blown way out of proportion.

I will strive to increase my income because more money is a good thing (if you treat it with respect). However, it is just one piece of the puzzle when it comes to living a fulfilling life. We’d all do well to remind ourselves of that regularly.

Photo Credit: Jordan Lloyd

Thanks for taking the time to explain this Tom.

I love seeing real numbers because it 1. is a great motivator and 2. provides context. If someone says “My business grew by 700% this month” it means nothing if they made $100 and then $700.

We shared numbers when we were paying off debt to help motivate people and be transparent.

And I agree with you that liquid cash is king. With greater liquidity you can be more nimble and act on new opportunities as they arise. And you’re able to withstand the ups and downs of your income.

I’ve enjoyed watching your content this year and am looking forward to what you’ll do in 2014!

Thanks Daniel!

Hi Tom,

thanks for explaining that again. I didn’t expect that. I also didn’t see the need for that second explaination. As I wrote at the other post: I respected your decision and in my point of view, you did correct, because you already didn’t leave us alone with it.

But that post impressivly shows me much more of your character, your formula for success and why I enjoy reading your blog: You really care about the opinion of your readers. Thank you!

Like Daniel alredy said: Numbers of the others are a big motivation. Hope to see some more on your blog soon. And if they can help me, I don’t care if they are your income reports or if they are just illustrating the development of one of your projects.

All the best,

Manuel

My pleasure Manuel. There will be no shortage of numbers in future posts, don’t worry 🙂

That was a fantastic breakdown that illustrates to people how to properly do income reports and break down surplus. Thanks for the great insight Tom!

My pleasure Jo!

Hey Tom,

I agree…to some extent.

Money isn’t everything.

But when you’re struggling, paying back loans or living in your mother’s house until you finally get on your feet, it sure as hell means a lot.

Even though many people talk a big game, I’m sure that they’d be happy living in relative comfort, and on a base level know that beyond a certain point money won’t make them happier.

However, when I reach that level, I’ll let you know 😛

Hey Daryl,

I agree entirely, but I’m not sure what you are disagreeing with in the post. After all, isn’t focusing on your total liquid capital the key to getting into a secure financial position?

Cheers,

Tom

All good points. I’ve definitely had similar issues with our income reports and was contemplating whether or not they should be done away with. For starters, they don’t really have anything to do with a travel blog and are much less relevant than say they are on your blog. Moreover, I’ve also had issues with what I was reporting in a given month and what was actually showing up in the bank accounts. It sounds pretty weird but we had months where we were taking in 10-15k and really it feels like our bank accounts aren’t increasing much at all! At least not as much as I would have expected, since those are sans business costs. As a result I signed up at personalcapital.com (.org?) to keep better track of my overall progress in, as you say, what really matters.

Hey Dave,

To be honest, I don’t think anyone should publish gross income reports — they can be woefully misleading. If you’re going to publish an income report, I heartily recommend you reveal your true (i.e. net) earnings.

Cheers,

Tom

Tom – our income reports are our net earnings (or at least have been for the last 4-6 months)

Ah I see, I wrote sans business costs, pardon my incorrect french – I meant WITH business costs included lol

Ah, okay!

Well, this post fascinates me, because as a longtime business finance reporter I’ve never heard the phrase “liquid capital” before. Is it the same as net profits? If so that’s certainly an important metric to track.

If you’re looking for a more sophisticated resource for tracking trends in your business, there’s a financial tool called ratio analysis that might help you — it looks at how long it takes you to get paid and how long it takes clients to pay you, and tracks how those figures are changing over time to determine your cash cycle.

As your business grows, you want to win the right to pay your bills slower and get paid by your clients faster to keep more money in your pocket at any given time and avoid having to incur debt or charge things on credit cards — that’s the trend you’re hoping to see.

Given the above, might be of interest to you.

Hey Carol, thanks for the suggestion!

This is what I mean by liquid capital: http://answers.yahoo.com/question/index?qid=20080826132917AABGHiu.

“I log these figures in a spreadsheet and compare the total to the previous month.”

Do you keep each month in a separate file or do you have a sheet for each month in your spreadsheet?

Nope, just a row for each month, that’s all!

Thanks for the reply Tom!

Do you keep track of expenses and/or debt & loans?

If we’re talking in terms of the business, no. There’s no debt or loans, and expenses are so low as not necessitate tracking. The only exception to that would be what I pay my writers, but that’s not really a cash flow issue as the gap between me paying them and getting paid myself is only a few days.

I’m disappointed that you are stopping the earnings reports! They were actually how I discovered your site and I enjoyed seeing how open you were with your reports and they gave me hope for someone who has just recently started working for myself whilst still at Uni.

Sorry to read that Elliot but I hope you will still find plenty of cause for hope!

I noticed for November and December you did your snapshot of your liquid capital figures on the 20th of each month.

Are you still doing them on the 20th? Why that day of the month specifically or why not if you’ve changed the day?

Yep! The 20th is convenient because its far enough away from any potential influencing factors, like big bills going out or payments coming in, etc.